After writing "Dividend ETFs vs. Bonds," I got to thinking about taxes. As we head into retirement, taxes will play a significant role in our decision-making.

Let's rerun the $500,000-401K scenario, but this time with a perspective focusing on taxes. Let's assume we are 66 years old and drawing social security.

What are qualified dividends? My favorite dividend ETF, Schwab High Dividend (SCHD), pays a qualified dividend (please reconfirm yourself).

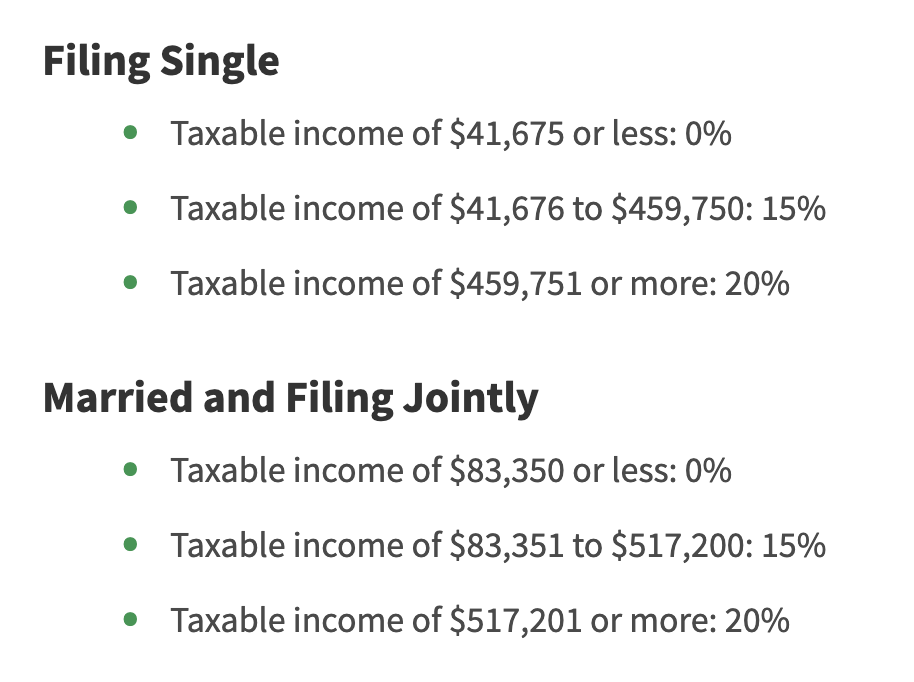

Qualified dividends give us preferred tax status. As you can see from the chart above, most of us will pay a 15% tax on our qualified dividends.

However, if you are drawing social security as a couple, you can get under $83,000. That would give you 0% on qualified dividends.

A social security example. Suppose you and your spouse earn $5,000 monthly in social security.

For this example, this is your only income. You take $500,000 from your 401K and purchase shares of SCHD.

This gives you an immediate income of $15,000/year at a 3% dividend yield. You are still under the threshold to pay 0% on your dividends. How amazing is that?

Non-qualified dividends. You will pay the ordinary tax rate on non-qualified dividends. This is your effective tax rate across your income bracket—the same rate you pay on interest from savings accounts and bonds.

It is essential to check the tax status of your dividend investments. I notice that corporations like McDonald's (MCD) and Starbucks (SBUX) usually pay qualified dividends.

When you enter Real Estate Investment Trusts and Bond ETFs, they usually pay non-qualified dividends. Let's review some of our options for bonds.

Tax implications from bonds. Keeping your $500,000 example, how can you lower your tax implications using bonds?

First and foremost, you can move to a state with no state income tax, like Florida—immediately lowering your tax liabilities.

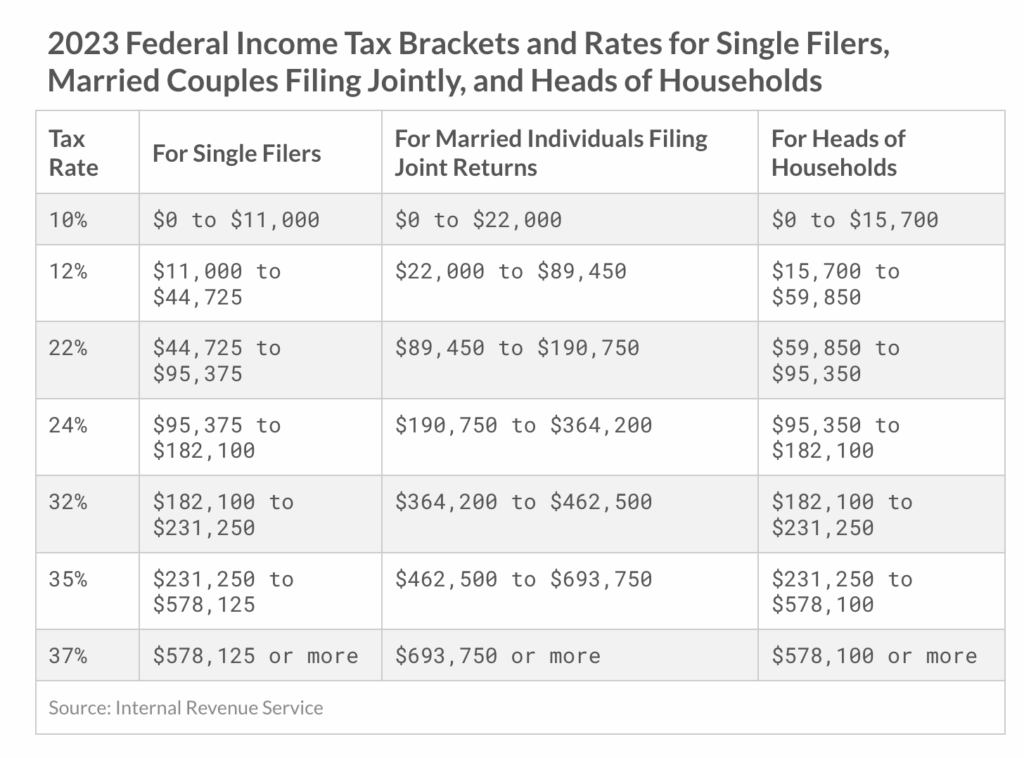

Next on the list is buying US Treasuries because they are exempt from state taxes. In our example, we would be in the 12% tax bracket.

Purchasing $500,000 in 30-Year Bonds (at 4.5%) would give us $22,500 in annual interest income. We would barely stay in the 12% bracket.

What if we purchased $500,000 in a municipal bond fund like Nuveen Tax-Free (NVG)? We would not pay taxes at the federal level from this fund, keeping you firmly in the 12% bracket.

Is it risky to put all your eggs in one basket? Putting all of your money into one municipal bond fund would be scary, so use that as an example only.

However, if you live in Florida, the dividends from NVG would be entirely Federal and State tax-exempt. I live in Florida and can confirm that this indeed does happen.

A combination of all of these techniques will serve us best. As much as we like staying in a low tax bracket, we still need income.

Putting it all together. We want to reduce your tax footprint as much as possible but don't want to avoid building a stream of income.

If your social security gives you enough income, consider switching your Dividend ETF to an index fund like SPY or QQQ.

SPY usually has a dividend yield of 1.5%, and QQQ is closer to 0.5%. This switch will reduce your tax liabilities from the 3% dividend yield—which typically means higher capital appreciation from index funds.

Series "I" and "EE" bonds. Other superb options are Series "I" and "EE" bonds. You can think of these as 30-year tax shelters.

Annually, an individual can put up to $10,000 into Series "I" Bonds and an additional $10,000 in "EE" Bonds. At age 66, I wouldn't recommend "EE" bonds because it takes 20 years for them to be effective.

You can put in $20,000 per year as a couple into Series "I" Bonds. This money grows tax deferred until you redeem your bond or it matures.

I love Series "I" Bonds because you can redeem them individually, extracting the exact amount of income you need to stay within your tax bracket.

With Series "I" Bonds, you couldn't withdraw your entire $500,000 at once and put it into these securities because of the annual limit.

Using all of the tools at our disposal. Therefore, if you put everything together, you can obtain great results.

With our $500,000, we can purchase some "I" Bonds, index funds, Dividend ETFs, municipal bonds, US Treasuries, and depending on our brackets, bond closed-end funds.

The more planning we do, the better we can survive inflation while keeping our tax bill low. You should monitor your tax implications continuously because they can suffocate you in retirement.

Consider starting a small business. Consider creating a small personal business that will give you some tax write-offs.

People love reading about dividends, bonds, and retirement planning, so that's a win. Starting a YouTube channel can help you lower your tax footprint.

Thinking outside the box will be your best tax tool going into retirement. Interest and dividends are tough to lower because everything is happening through your social security number.

Conclusion. We can improve our quality of life by thinking of ways to increase our revenue outside of paper income (stocks and bonds).

My book business gives me some tax relief on buying things like computers and Microsoft Office subscriptions.

I plan on making a ton of money in retirement, so I am considering ways to reduce my tax footprint today. In the end, planning is an essential tool for success.

I love the simplicity of dividend ETFs. In fact, SCHD just paid me a dividend a couple of days ago. I also love Series "I," municipal, and 30-year Treasury Bonds.

Together, I am building a powerful income-generating nest egg. These securities will also help me build generational wealth within my family. It is a win for everyone, even Uncle Sam. Good Luck!

- PDF of the Month: Don't Gamble with Retirement 10 (Free 419-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don't Gamble with Retirement 10 (Free 419-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer's Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don't Gamble with Retirement 10 (Free 419-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

No comments:

Post a Comment